NON-DOMESTIC RATES BILL CHANGES TO LEGISLATION IN SCOTLAND

Home / Insights / Non-domestic rates (Scotland) bill changes to legislation

On 5th February The Scottish Parliament passed into Legislation The Non Domestic Rates (Scotland) Bill.

This new Primary Legislation provides the necessary framework for the changes to the Scottish Non-Domestic Rates System and more importantly provides the Scottish Assessors Association and Local Authorities with increased powers to obtain information and introduces substantial fines for noncompliance.

INCREASED ASSESSOR POWERS AND THE INTRODUCTION OF CIVIL PENALTIES

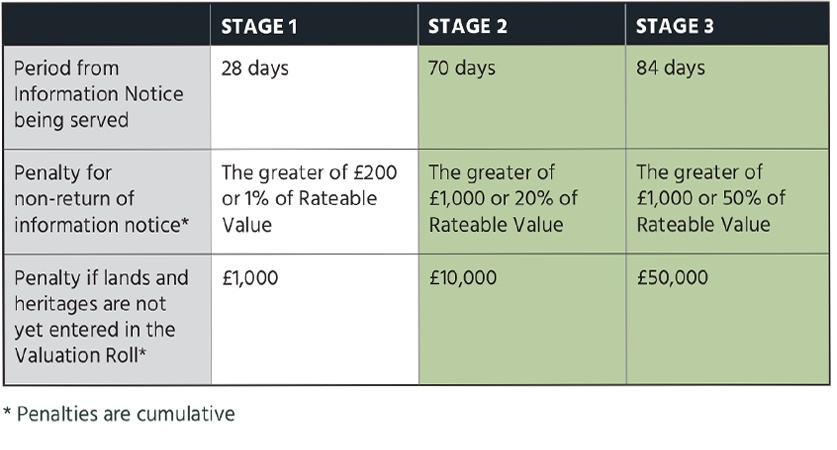

From the 1st April 2020 penalties can be issued for non-return of information in respect of a Rent Return of Information, Cost Return of Information or Trade Return of Information.

The Assessors may issue a form to:

any person who the Assessor thinks is a proprietor, tenant or occupier of lands and heritages; and/or

any other person who the Assessor thinks has information which is reasonably required for this purpose.

The timescales and penalties for return of such requests are substantially more onerous than in England and Wales and are summarised below.

It is imperative that any request received is directed to the appropriate person within your organisation and are acted on within the statutory time limit.

Graham Howarth

IMPORTANT ACTION REQUIRED ON RECEIPT OF A REQUEST

We have serious concerns that the level of penalties are excessive in relation to the nature of the request but despite industry wide lobbying they have been passed into the legislation.

It is therefore imperative that any request received is directed to the appropriate person within your organisation and are acted on within the statutory time limit.

We can assist you with the return of these forms, but you will need to be able to provide us with any information required in order to allow us to comply with the strict time limits in place. As a result of these legislative changes an additional fee may be required to cover our time in completing these forms to the Assessor within the tight timescales provided.

The party to whom the form is issued will be liable for any fines for non-completion which are cumulative.

INCREASED LOCAL AUTHORITY POWERS

In addition to the increased powers provided to the Scottish Assessors, Local Authorities also have been provided with increased powers to collect business rates and information from ratepayers.

The timescales and penalties do differ from that provided to the Assessors.

The Non-Domestic Rates (Scotland) Bill provides the Local Authorities to commence debt recovery quicker. Where no payments are made, the Local Authorities can apply to recover the full amount due for non-payment. This will commence earlier in the financial year (June/July) in comparison to October as currently in place.

Local Authority information notices may take the form of information requests for details relating to the paying, collecting and updating etc required by Local Authority finance departments for Non-Domestic business rates administration/billing.

These are major change to the powers provided to the Scottish Assessors, Local Authorities and we will have to wait to see how ready they are to exercise their powers to issue fines. It is important that they are not given the opportunity to test these powers and that your teams are aware of the importance of acting swiftly on receipt of a request.

We use cookies to give you the best possible experience. We can also use it to analyze the behavior of users in order to continuously improve the website for you. Data Policy

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.